The Metal the Rally Forgot

Four consecutive supply deficits, less than three months of above-ground stock, and a gold-to-platinum ratio still near historic extremes — the case for platinum at current prices.

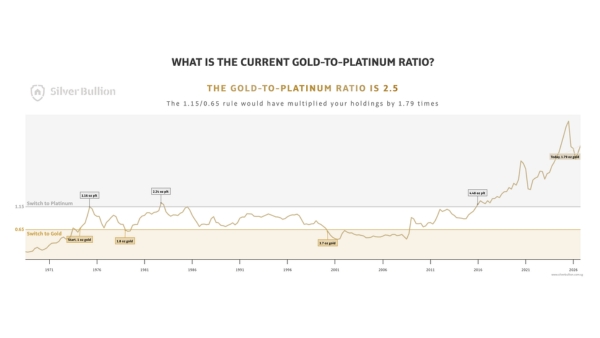

For most of the four decades before 2015, platinum cost more than gold. Today, with gold around $4,120 and platinum around $1,630 per ounce, one ounce of gold buys roughly two and a half ounces of platinum. Platinum has hardly stood still — it more than doubled between early 2025 and its January 2026 peak above $2,700 — yet after a sharp retracement, the relationship between the two metals remains inverted to a degree with few historical precedents.

Anomalies of this size usually have one of two explanations: either the world has permanently changed, or the price has not yet caught up with the world. The evidence increasingly points to the second.

Track this in real time on our Gold-to-Platinum Ratio page.

The World Platinum Investment Council's latest Platinum Quarterly, published in May, forecasts a fourth consecutive annual supply deficit in 2026 — 297,000 ounces — following a record shortfall of nearly 1.2 million ounces in 2025. The cumulative deficit over the past three years alone approaches 3 million ounces, in a market whose entire annual supply is only around 7.4 million.

Deficits are filled from inventory — and the inventory is running down. Above-ground stocks have fallen by roughly half since their 2022 peak and are projected to end 2026 at about 1.75 million ounces: less than three months of global demand cover, the lowest since the WPIC's records began. The market has already offered a preview of what that means in practice: platinum lease rates — the cost of borrowing physical metal — reached record levels during 2025, a classic symptom of physical tightness.

|

Key Insight

A thick inventory buffer turns deficits into gradual price adjustments. A thin one turns supply surprises into physical availability problems. At under three months of cover, the buffer is thin.

|

In most commodities, a doubling of price calls forth new supply. Platinum's response has been telling: mine supply for 2026 is projected to be roughly flat, and recycling — the only flexible source — is expected to grow just 9%. A new platinum mine takes seven to ten years from discovery to production; projects that are coming online will take up to several years to start producing platinum.

The supply base is also remarkably concentrated. South Africa alone accounts for roughly 70% of mined platinum, and together with Russia and Zimbabwe controls about 90% of primary platinum-group-metal supply. Each carries its own risks: Russia's Nornickel reported platinum output down 26% year-on-year in the first quarter, and Zimbabwe banned exports of unrefined critical minerals in April. Gold is mined on every continent; platinum, in practice, is mined in three places, none of them without complications.

Meanwhile demand has quietly broadened. Hybrid vehicle production — which uses full catalyst loadings — is growing at double digits even as pure combustion declines. Industrial demand is forecast to rise 9% this year, drawn by glass capacity expansion and, increasingly, by technologies underpinning AI infrastructure. And physical investors have noticed: bar and coin demand is forecast to grow 27% in 2026, across every region.

One honest caveat is worth stating plainly: platinum is a smaller, more industrial and more volatile market than gold. The metal fell from above $2,200 to near $1,900 in five trading sessions this May, when interest-rate expectations shifted. Platinum now trades roughly 40% below its January peak — while the WPIC's deficit forecast, published in May after that retracement, is unchanged in direction. Sentiment repriced in weeks; the fundamentals did not. Platinum is not a substitute for a core gold position; it is a complement to one.

But for the long-term holder, the arithmetic is unusual. Unlike gold — of which nearly every ounce ever mined still exists above ground — most platinum ever produced has been consumed. Annual mine supply is roughly one-twentieth that of gold. The buffer between demand and scarcity now covers less than a quarter of a year. And the price, despite everything above, still buys less than half the gold it did for most of living memory.

Availability is the practical question in a physically tight market — and we have addressed it directly. As a partner of World Platinum Investment Council, Silver Bullion is now obtaining platinum products directly from refiners. We now source from one of the world's largest primary platinum producers, and we maintain good in-stock availability of platinum bars and coins in Singapore. Our team has just returned from Shanghai Platinum Week, the industry's principal Asian gathering held from 6-10 July, where the tightness described above was very much the conversation.

Platinum stored under S.T.A.R. Storage carries direct legal title to specific, serial-numbered bars — tested on intake, insured, and never on our balance sheet. As always: own the metal, not the promise.

Platinum of qualifying purity is an Investment Precious Metal in Singapore and therefore GST-exempt. For those building a position gradually, S.T.A.R. Platinum Grams offers fractional legal ownership of specific platinum bars from as little as 0.01 grams — and stored platinum can be collateralised through our secured lending platform without ever leaving the vault. Platinum bars and coins are available in our platinum shop.

Regards,

Gregor Gregersen

Founder & CEO of Silver Bullion Pte Ltd

|

Special Offer

Best Price in the Market

|

||

| Get platinum bars at a premium of just US$62/oz over spot, one of the lowest premium and tightest spread available. Lock in your position before the price moves. |

||

|

||

|